posts / Machine-readable data 101

Machine-readable data 101:

guidance on European parties and foundations

— Louis Drounau, EDCS founder

20 May 2026 — The latest Regulation on European parties and foundations requires data to be published in "open, machine-readable format". This is a welcome step forward, but can be difficult to implement. EDCS offers a comprehensive guide to improve transparency on European parties and foundations.

Transparency in political finance is a key principle of modern democracy: political parties representing citizens are granted a central role in our political systems and, in exchange, they are required to be transparent, including on their funding and spending. This principle applies to European political parties as it does to any other parties.

Adopted in December 2025, Regulation 2025/2445 includes a new provision requiring that data on European parties and foundations be in "open, machine-readable format". This requirement concerns data reported by these entities, as well as data later published by the Authority for European political parties and European political foundations (APPF) and the European Parliament's Directorate General for Finance (DG FINS). This is an important step forward to ensure transparency and facilitate civil society's oversight of political finance.

However, in order to have the desired impact, this provision must be implemented properly. In this guide, we will go through the meaning of "open data" and "machine-readable formats", see how this requirement can be implemented to achieve needed transparency, and provide real-life examples of machine-readable data.

If you are already familiar with reporting requirements, you can skip straight to the section on open, machine-readable data or to our our guidance.

Recommendations

- Choose the most suitable file format

- Structure your data

- Check your content to avoid pitfalls

- Focus on transparency instead of documents

Legal framework

In December 2025, Regulation 2025/2445 entered into force, replacing Regulation 1141/2014. This new framework updated legal provisions on a number of topics, but seldom changed the section relating to transparency. Its main innovation, however, was the insertion of a requirement to report and publish data in "open, machine-readable format". In particular, the Regulation contains the following reasoning:

(51) For reasons of transparency, and in order to strengthen the scrutiny and the democratic accountability of European political parties and European political foundations, information considered to be of substantial public interest, relating in particular to their statutes, membership, financial statements, donors and donations, contributions and grants received from the general budget of the Union, as well as information relating to decisions taken by the Authority and the Authorising Officer of the European Parliament on registration, funding and sanctions, should be published in a user-friendly, open and machine readable format. Laying down a regulatory framework to ensure that such information is publicly available is the most effective means of promoting a level playing field and fair competition between political forces, and of upholding open, transparent and democratic legislative and electoral processes, thereby strengthening the trust of citizens and voters in European representative democracy and, more broadly, preventing corruption and abuses of power.

In the section below, we will review the transparency requirements under the applicable Regulation, as well as the modalities for the publication of this information. In particular, we will focus on recurring elements (such as public and private funding or membership), and not elements to be submitted for registration as a European party or foundation and their occasional updates (such as statutes and relevant provisions therein).

Transparency requirements

For European parties and foundations

The first step is for European parties and foundations (the "reporting entities") to report information to the APPF and DG FINS, in line with their respective remits.

Article 28.1 on Accounts, reporting and audit obligations lists the following items that reporting entities are required to submit within six months of the end of the calendar year (colouring added):

- their annual financial statements and accompanying notes, covering their revenue and expenditure, assets and liabilities at the beginning and at the end of the financial year, in accordance with the law applicable in the Member State in which they have their seat;

- an external audit report on the annual financial statements, covering both the reliability of those financial statements and the legality and regularity of their revenue and expenditure, carried out by an independent body or expert;

- the list of donors and contributors and their corresponding donations or contributions reported in accordance with Article 25(2), (3) and (4).

Article 25 on Donations, contributions and self-generated resources, referred to above, states that:

2. European political parties and European political foundations shall, at the time of the submission of their annual financial statements in accordance with Article 28, also transmit a list of all donors with their corresponding donations, indicating both the nature and the value of the individual donations. This paragraph shall also apply to contributions from member parties from the Union and member organisations from the Union, to contributions exceeding EUR 1 500 made by individual members of European political parties and European political foundations and to self-generated resources of European political parties and European political foundations. [...]

3. Donations received by European political parties and European political foundations within six months prior to elections to the European Parliament shall be reported on a weekly basis to the Authority in writing and in accordance with paragraph 2.

4. Single donations the value of which exceeds EUR 12 000 that have been accepted by European political parties and European political foundations shall be immediately reported to the Authority in writing and in accordance with paragraph 2.

5. For all donations the value of which exceeds EUR 3 000 per year and per donor, European political parties and European political foundations shall request that such donors provide the necessary information so that they can be properly identified. European political parties and European political foundations shall transmit the information received to the Authority upon its request.

Additionally, Article 28 mentions that:

2. Where expenditure is implemented by European political parties jointly with national political parties or by European political foundations jointly with national political foundations, or with other organisations, evidence of the expenditure incurred by the European political parties or by the European political foundations directly or through those third parties shall be included in the annual financial statements referred to in paragraph 1. [...]

4. European political parties and European political foundations shall provide any information requested by the independent bodies or experts for the purpose of their audit.

Finally, Article 11 on Examination of the application and decision of the Authority requests that:

6. By 30 September each year, the updated list of member parties of a European political party, annexed to the party statutes in accordance with Article 4(2), shall be sent to the Authority, together with the standard formal declaration, using the template set out in Annex I, if a new member party has joined. [...]

This information, together with what the APPF and the European Parliament themselves decide (including sanctions and public funding decisions), forms the basis of what will later be published.

For European institutions

Information reported to the APPF and DG FINS holds a double purpose: it enables these institutions, as well as external auditors and law enforcement bodies, to carry out their compliance monitoring work, and it allows for the consistent publication of this information, instead of leaving this to the reporting entities themselves.

Article 39 guides these publication requirements and states that:

1. The European Parliament, or the Authority, in accordance with the distribution of their responsibilities under this Regulation, shall make public in an open, machine readable format on a website created for that purpose, the following: [...]

- an annual report with a table of the amounts paid to each European political party and European political foundation, for each financial year for which contributions have been received or grants have been paid from the general budget of the Union;

- the annual financial statements and external audit reports referred to in Article 28(1), and, for European political foundations, the final reports on the implementation of the work programmes or actions;

- the names of donors and their corresponding donations reported by European political parties and European political foundations in accordance with Article 25(2), (3) and (4), [...]; the total amount of minor donations and the number of donors per calendar year are also to be published;

- the contributions referred to in Article 25(9) and (10) and reported by European political parties and European political foundations in accordance with Article 25(2);

- the self-generated resources referred to in Article 25(13) and reported by European political parties and European political foundations in accordance with Article 25(2);

- in the six-month period prior to the elections to the European Parliament, the weekly reports received pursuant to Article 25(3); [...]

- an updated list of members of the European Parliament who are members of a European political party.

2. The Authority shall make public the list of member parties of a European political party, as annexed to the party statutes in accordance with Article 4(2) and updated in accordance with Article 11(6), as well as the total number of individual members.

In addition to the above, the Regulation requires the publication of other documents, decisions on sanctions, the annual report of the APPF, or its draft budget.

Publication modalities

Historically, the Regulation has never been really precise regarding the publication modalities for the information it listed. Over time, the APPF and DG FINS have drawn up forms for the reporting of specific information, and these forms would be e-mailed back by reporting entities. More recently, an upload platform allowed for more secure communications and ensured that documents were available to both institutions.

As indicated, the biggest innovation regarding transparency in the latest iteration of the Regulation is the request to provide specific information in "open, machine-readable format". This is mentioned in three parts of the Regulation:

- Recital 51: applies to information "considered to be of substantial public interest", which should be published "in a user-friendly, open and machine readable format", including "[relating to] their statutes, membership, financial statements, donors and donations, contributions and grants received from the general budget of the Union, as well as information relating to decisions taken by the Authority and the Authorising Officer of the European Parliament on registration, funding and sanctions". This is very broad scope.

- Article 28.1: applies to annual financial statements and accompanying notes, the external audit report, and the list of donors and contributors and their corresponding donations or contributions. This article also states that a copy of this submission should be sent, "in an open, machine readable format", to the APPF and to the National Contact Point of the Member State of entities' seat.

- Article 39.1: applies to the documents listed above, to be published by the APPF or DG FINS.

While a step in the right direction, the above legal provisions are not without issues. For instance, while recital 51 seems to cover most information reported by parties and published by institutions, the narrower scope of the subsequent uses casts a doubt regarding the way this will be implemented.

The impact of this new provision will depend on its implementation.

Information to be reported by parties and foundations on joint expenditure with national parties, mentioned in Article 28.2, references paragraph 1 which seems to imply that information should be reported under the same modalities. However, the "list of member parties of a European political party" mentioned for publication by the APPF is listed under Article 39.2, and therefore does not fall under the explicit requirement found in Article 39.1.

More generally, the impact of these provisions will depend on their implementation. For reference, the 2018 revision of Regulation 1141/2014 already required that national member parties display, on their website, the logo of their European party of affiliation "in a clearly visible and user-friendly manner", as a pre-requisite for public funding. However, European Democracy Consulting's 2021 Logos Project found that "85% of member parties do not display the logo of their European party of affiliation in a “clear and user-friendly” manner"; no European party was ever denied its public funding on these grounds.

It is therefore particularly important for institutions to properly understand the technical meaning and implications of this provision, and to ensure its proper implementation.

Basic considerations

The ink had not yet dried on the new Regulation when the European Parliament made its first attempts to navigate this new provision.

On 23 February 2026, DG FINS circulated a letter to reporting entities to underline the legal novelties of the new Regulation. Among others, the table annexed to this letter stated that "Annual financial statements, external audit reports and lists of donors/contributors have to be submitted in an open, machine-readable format. Example of machine-readable format: PDF with fully selectable and searchable text." This is despite PDF specifically not being a machine-readable format.

Later, in May 2026, DG FINS added comma-separated values (CSV) versions of its tables listing the amounts of public funding received by European parties and foundations. However, it quickly appeared that the document was merely an Excel file that has merely been saved as CSV files. While using the right format, these files lacked the required structure of machine-readable data, and many of its values had been corrupted as zeroes for thousands were confused with decimals. As a result, the file was unexploitable, defeating the purpose of a machine-readable file.

Of course, we commend DG FINS for being pro-active and for seeking to ensure compliance with new obligations, yet these two examples highlight the difficulty to quickly implement this requirement as well as the importance of a proper implementation to reach the intended goal.

For this, we will go through the concepts of open and machine-readable formats.

What is a file format?

The Open Data Handbook's glossary defines a file format as follows:

The description of how a file is represented on a computer disk. The format usually corresponds to the last part of the file name (‘extension’), e.g. a file in CSV format might be called schools-list.csv. The file format refers to the internal format of the file, not how it is displayed to users. E.g. CSV and XLS files are structured very differently on disk, but may look similar or identical when opened in a spreadsheet program such as Excel.

Some formats are considered open, while others are not; some formats are machine-readable, while others are not. The legal requirements introduced in Regulation 2025/2445 requires the reporting and publication of data in a format that is both.

What is open data?

There are various definitions of open data, open formats, and open standards.

The European Data Portal defines "Open standards" as follows:

Generally understood as technical standards that are free from licencing restrictions. They can also be interpreted to mean standards that are developed in a vendor-neutral manner.

Meanwhile, the Open Data Handbook defines "Open Data" as follows:

Data is open if it can be freely accessed, used, modified and shared by anyone for any purpose — subject only, at most, to requirements to provide attribution and/or share-alike. Specifically, open data is defined by the Open Definition and requires that the data be

- Legally open: that is, available under an open (data) license that permits anyone freely to access, reuse and redistribute

- Technically open: that is, that the data be available for no more than the cost of reproduction and in machine-readable and bulk form.

The Open Definition referred to above is a standard first released in 2005, and "sets out under what conditions data and content is open".

OpenDefinition.org, run by the Open Knowledge Foundation states that "Open means anyone can freely access, use, modify, and share for any purpose (subject, at most, to requirements that preserve provenance and openness)." Further, it states that an open work

must be provided in an open format. An open format is one which places no restrictions, monetary or otherwise, upon its use and can be fully processed with at least one free/libre/open-source software tool.

Formats that are not open are therefore considered "proprietary", which the Open Data Handbook defines as follows:

A proprietary file format is one that a company owns and controls. Data in this format may need proprietary software to be read reliably. Unlike an open format, the description of the format may be confidential or unpublished, and can be changed by the company at any time. Proprietary software usually reads and saves data in its own proprietary format. For example, different versions of Microsoft Excel use the proprietary XLS and XLSX formats.

Finally, formats can also evolve over time. For instance, Open Data Handbook's definition of "PDF" states that "originally a proprietary format of Adobe Systems, PDF has been an open format since 2008."

Common examples of proprietary formats include .docx, .xlsx, and .pptx by Microsoft, .pages, .numbers, and .key by Apple, and .gdoc, .gsheet, and .gslides by Google.

By contrast, examples of open formats includes Comma-Separated Values (.csv), the Open Document Format (.odt for text, .ods for spreadsheets, and .odp for presentations), the JavaScript Object Notation (.json), or the Extensible Markup Languag (.xml).

For reference, when browsing the European Parliament's list of MEPs, either the full list or subsections based on member state, political group, or committee, the website provides an option to export the list in question both as a PDF or as an XML document.

What is machine-readable data?

As for open data, there are various defintions for machine-readable data, and it is useful to read a few. The Open Data Handbook defines "machine-readable" as follows:

Data in a data format that can be automatically read and processed by a computer, such as CSV, JSON, XML, etc. Machine-readable data must be structured data.

In turn, "structured data" is

data where the structural relation between elements is explicit in the way the data is stored.

Data organised in columns is structured data, so is data organsised as "property-value", where one element provides a property ("amount", "hair colour") and another the associated value ("3000", "brown").

By contrast, word-processing documents or PDFs "reflects the positioning of entities on the page, not their logical structure", which hampers or prevents automatic analysis.

Meanwhile, the European Data Portal defines "machine-readable" as follows:

Machine-readable data are data in a format that can be interpreted by a computer program. There are two types of machine-readable data:

- human-readable data that are marked up so that they can also be understood by computers, for example, microformats and RDFa.

- data formats intended principally for computers, for example, RDF, XML and JSON.

In practical terms, machine-readability therefore means that data is either presented in columns without customised layout, bold or italicised fonts, images, or hyperlinks (in CSV or ODS files), or as "property-value" pairs (in XML or JSON files).

|  |

|---|

Implementation

We know which data should be provided in open, machine-readable format, and we have a clearer understanding of what this requirement means. Now, let us see in practice how to transition from the current approach to one that complies with the legal requirement.

Applicability

We saw above that, while the openness of file formats applies to any use, machine-readability is particularly applicable to data, and slightly less so to text. We can therefore distinguish two cases:

- Data-based documents: these include the amounts of public funding paid to European parties and foundations, lists of donors and contributors, lists of members, etc. These documents must be in an open file format of structured data, and are further discussed below.

- Text-based documents: these include statutes, financial statements, audit reports, etc. These documents must be in an open file format from which content can easily be extracted, such as OpenDocument Text file (.odt).

To be clear, the Regulation requires the publication of data in open, machine-readable format, but it does not prevent its publication in other formats. Documents, especially text-based ones, can therefore always be published in PDF alongside their machine-readable equivalent.

Which formats to choose from?

We have seen that simply requiring data to be provided in "open, machine-readable format" does not prescribe a specific file format, and this flexibility in the law is welcome. Let us discuss the available formats for structured data.

The main formats available are CSV, JSON, and XML, and their suitability depends on the use-case at hand:

- CSV is the simplest format and is designed for tabular data — that is, data organised as a table. It is easy to read and edit, and directly editable in all spreadsheet-compatible software;

- JSON and XML are "property-value" structured format and are more compatible with databases; JSON is simpler in its structure, while XML can represent more complex data structure; however, these are not as straightforward to edit.

|  |  |

|---|

Since the data that already exists is in tabular form and stored in Excel files, the most suitable format is likely CSV — although, as we will see later, we do not need to be limited to this choice.

Understanding the CSV format

A CSV file is merely a text file where commas, or another specific sign, mark column boundaries, and where line breaks mark row boundaries. No sheets, no layout, no images.

If you open a CSV file with a spreadsheet editor (such as LibreOffice Calc or Microsoft Excel), data will display in columns; but if you open it with a text editor (such as LibreOffice Writer or Microsoft Notepad or Word), the same data will display in lines, separated by the chosen sign — usually a comma or semi-colon.

Rendering of a CSV file in a spreadsheet editor:

| european_party | full_name | activity_status | date_activity_start | date_activity_end |

|---|---|---|---|---|

| ALDE | Alliance of Liberals and Democrats for Europe Party | Active | 1976 | present |

| ECPP | European Christian Political Party | Active | 2002 | present |

Rendering of a CSV file in a text editor (with semi-colons as separators):

european_party;full_name;activity_status;date_activity_start;date_activity_endALDE;Alliance of Liberals and Democrats for Europe Party;Active;1976;presentECPP;European Christian Political Party;Active;2002;present...

A CSV file therefore only has two simple rules: one line is one record, and a specific sign separates columns.

Transitioning to CSV

Because machine-readable data is structured data, merely saving an Excel document as CSV is not sufficient to meet the legal requirement of machine-readability. Instead, data must be structured.

The guiding principle to structure data is that

each line is a record relating directly to the goal of the table that should be complete on its own.

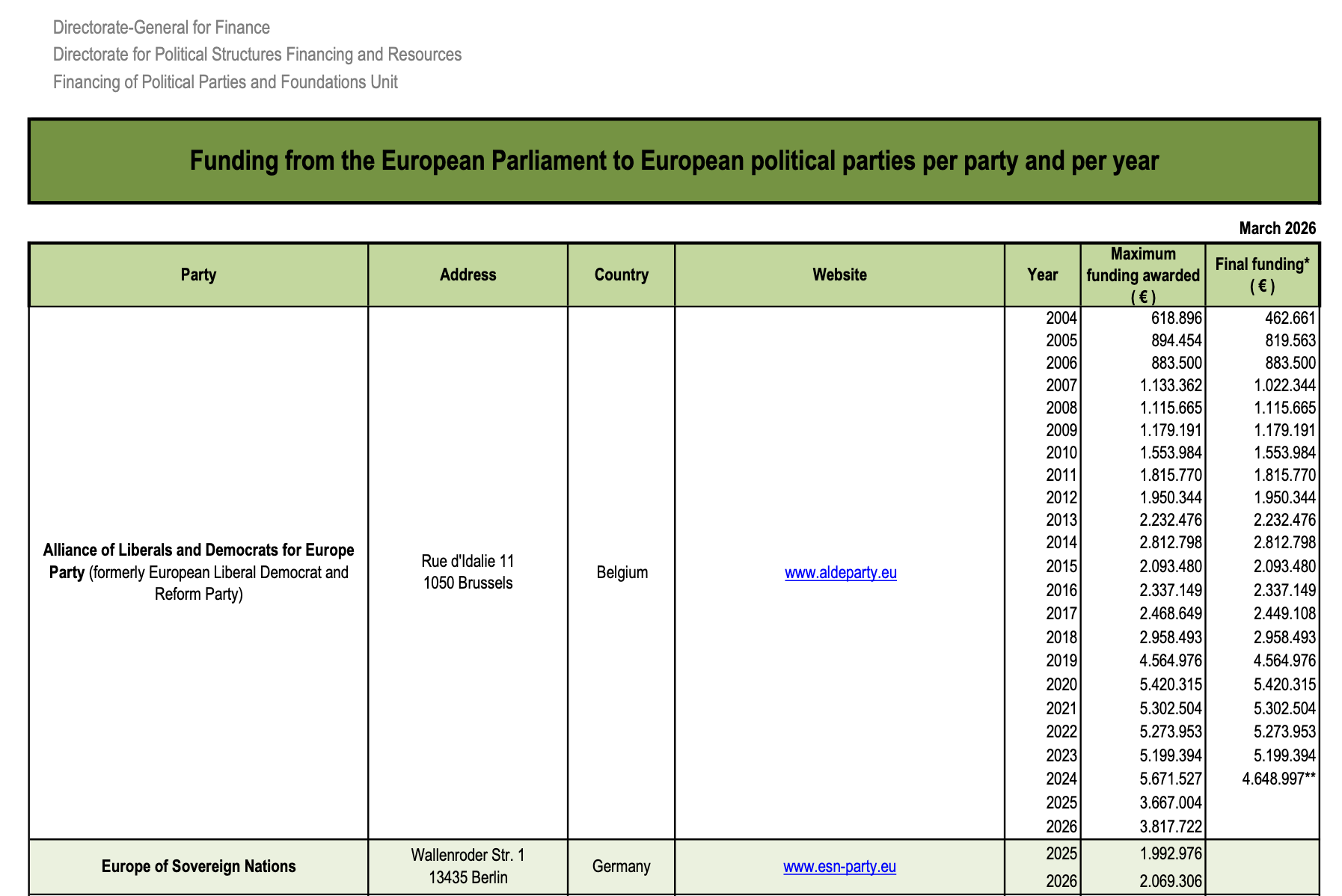

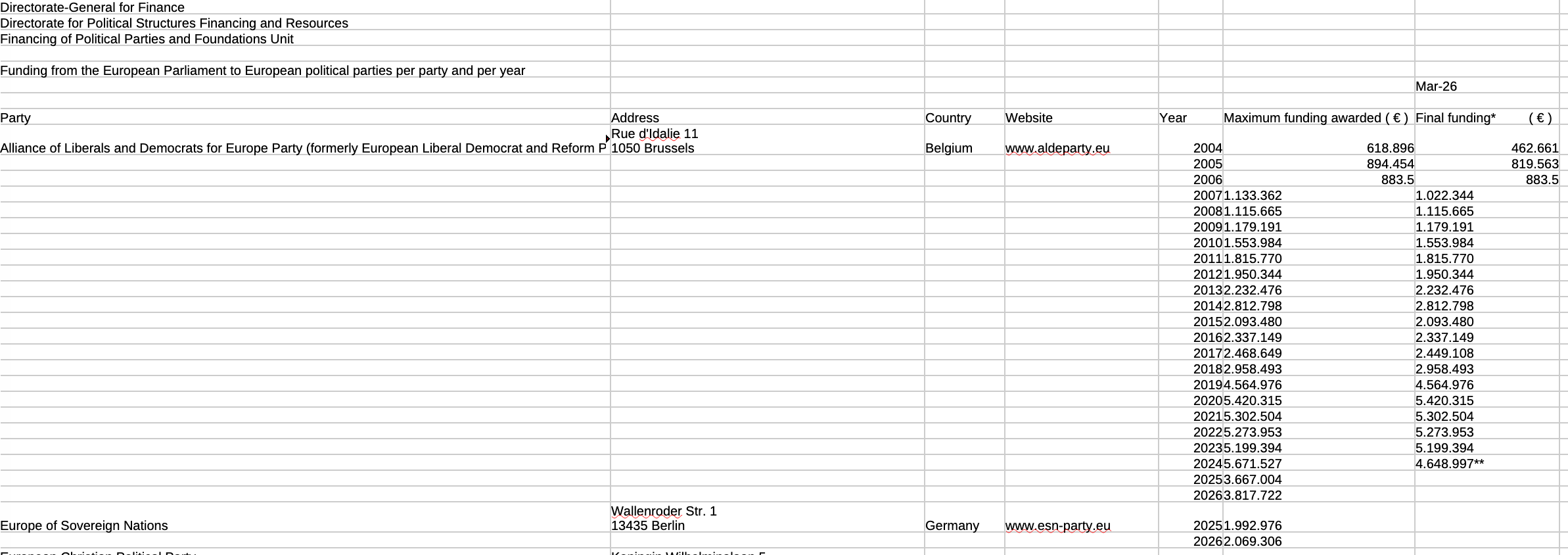

Consider the PDF file published by DG FINS listing the amounts of public funding awarded to European political parties (itself exported from a source Excel file) with the CSV that was subsequently published.

| ➜ |  |

|---|

We see that the layout found in the PDF file, with the party name, address, country and website mentioned once for each European party, is also found in the CSV. Likewise, the title, the reference to the publisher of the document (DG FINS), and the date are found at the top of the CSV table.

As a result, many lines in the CSV file are not consistent with the guiding principle:

- some lines are not actual records of data, as they do not include amounts;

- some records are not complete on their own, as they include amounts and dates but not a party name; and

- some records are not readable, as the amount contains two dots (originally used as thousand separators).

Additionally, we see that amounts that seem to display properly (such as "618.896") are actually misread, with the thousand-separating dot understood as a decimal-separating dot. This is clear from "883.500" being automatically simplified as "883.5".

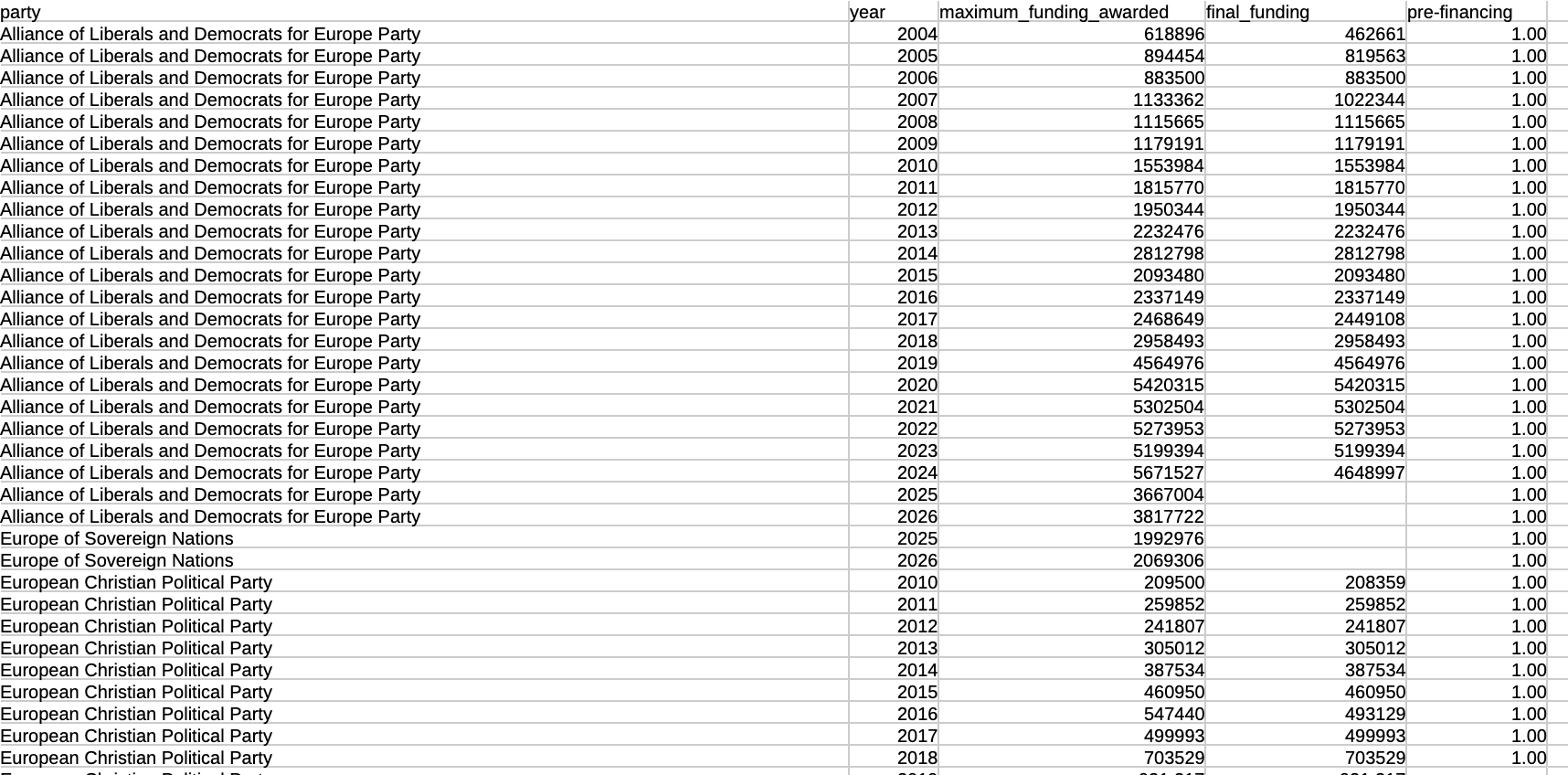

Transitioning the above data from the source Excel to structured data requires the following steps:

- remove all lines that are not actual records: this includes the title, name of the publisher, and date; if needed, this information can be placed in the name of the file itself;

- remove all blank lines: these are not records and do not belong in structured data;

- remove notes marked with asterisks: if these relate directly to the record itself (for instance, in the case of public funding, the fact that the amount was provided as pre-financing), a dedicated column can be inserted to include this information (with the percentage of pre-financing as a value from 0 to 1); if the note does not relate to the record at hand, it can be included in accompanying notes instead;

- ensure that each line contains all the necessary information to be complete on its own: a record of public funding requires, at least, the name of the receiving party, the year, and the amount received, and all three fields must feature on all lines (in the example above, the presence of the maximum grant, which is known before, means that some lines do not yet have the final amount received);

- display raw data: numbers should not contain thousand separator, percentage signs, or currency signs; for instance, "1.234.567,89" should be written as "1234567.89" (and "46M" should be "46000000.00"), with a dot marking the decimal; "87 %" should be "0.87"; and "€1000" should be "1000.00" — if needed, precisions regarding the type of data can be included in the name of the column;

- remove data not related to the record: in the example above, records on public funding include European parties' address, country, and website; this information relates to the party itself and not to the record of public funding; instead of duplicating this information in all records of the same party, it should be removed and placed in a dedicated structured data table focusing on reporting entities, where each line will be a record of an entity and columns will list their name, acronym, address, member state, website, etc.

- ensure that each field only contains its value: in the example above, names sometimes include a party's former name; if this information is needed, it should be placed in a different column — in this case, this column should be in the separate structured data decidated to reporting entities.

In additional, best practices for clear data files include:

- avoiding capital letters in column headers;

- replacing spaces with underscores in column headers; and

- adding unique identifiers to records: this is useful to quickly identify an entry (donation, membership, etc.), when an entity changes its name (European or national party, company, etc.), or when names are reported differently ("Microsoft", "Microsoft Belgium", "Microsft S.A.", "Microsoft SA" can all be the same entity).

The images below show how DG FINS's proposed CSV file should be reviewed following best practices on structured data:

| ➜ |  |

|---|

Common pitfalls

Due to the nature of CSV files and the absence of data validation, some pitfalls must be looked out for.

Firstly, when converting a spreadsheet into CSV or saving as CSV, leading zeroes may be removed. For instance, "00123" may become "123". While this is welcome for numbers, it may adversely affect other fields, such as identifiers.

Solution: ensure that fields that are not numbers are clearly formatted as "Text" when using LibreOffice or Excel.

Secondly, each file format is encoded using a specific set of characters. In case of mismatch between the characters used to encode the CSV file and the characters expected by the editing software, some characters may be replaced with sequences such as � or Ã.

Solution: to avoid this, ensure that you encode your CSV file in UTF-8, which is the expected character encoding for most applications. This is likely to already be the default in your software.

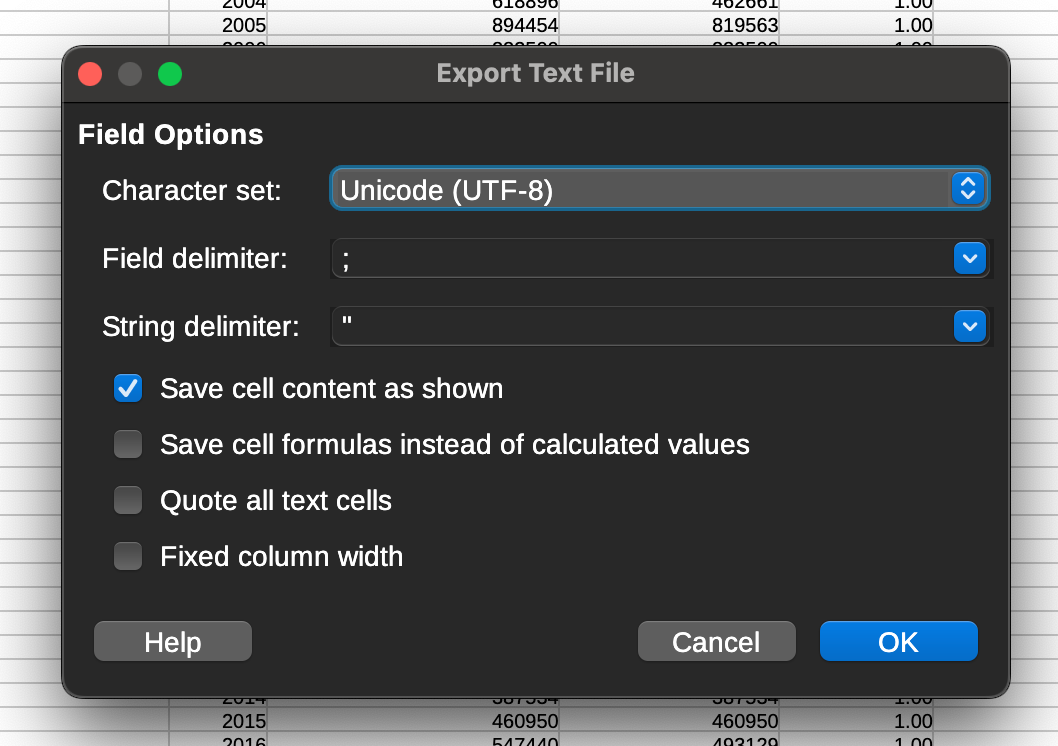

Thirdly, if a value contains the sign used to separate columns (such as a comma or semi-colon), this will unwantingly split the value in two columns. Here is an example with a value contains a comma:

| ➜ |

|

|---|

Solution: consider using a separator that is less likely to feature in your values (semi-colons may be better than commas), and choose a string delimiter which will clearly separate the values from each other, such as double quote (").

| ➜ |

|

|---|

All these options are usually found in the settings of the CSV file or when exporting a regular spreadsheet, such as an ODS file, into CSV. Below is the export settings window of LibreOffice upon saving an ODS as CSV.

Going further

We have now seen how to comply with Regulation 2025/2445's new "open, machine-readable requirement" by transitioning text-based document to open, editable formats, such as ODT, and data-based documents to open, structured data formats, especially CSV.

However, there are ways to further ensure transparency, and even facilitate the work of reporting entities and institutions.

Working with multiple sheets

As plain text files, CSV files cannot contain several sheets the way regular spreadsheet documents can. However, collating several sheets into a single document may be useful to centralise data management and to link data across sheets with formulas.

A possible way forward is to use open spreadsheet files, for instance in ODS format, containing several sheets, each formatted as structured data. This way, a single file can contain much more detailed data, but each sheet can be exported to CSV without changes to its content.

For instance, the APPF could have a single file containing the following sheets:

- general information on the content of the next sheets, relevant URLs, contact information, and the update date;

- information on European parties and foundation, including their type (party/foundation), acronym, former name, address, website, registration date, deregistration date, etc.;

- information on national member parties, including the name in local language and English, the European party of affiliation, the date of start of affiliation, the date of end of affiliation, etc.;

- information on donors, including their name, country, national legal identifier, type (natural/legal person), single identifier in APPF records, etc.; and

- information on donations, including the date/year, the APPF identifier of the donor, the receiving entity, the amount, the nature of the donation (financial/in-kind), etc.

Publish data on the European Data Portal

Now that the data is provided in open, machine-readable format, it can be easily exploited by third-parties, including the media and civil society organisations.

A useful way to make this data available is to publish it on the European Data Portal, which describes itself as "a central point of access to European open data from international, European Union, national, regional, local and geodata portals." Among others, this portal seeks to "promote and support the release of more and better-quality metadata and data by the EU’s institutions, agencies and other bodies, and European countries, enhancing the transparency of European administrations."

Providing data on European political parties and foundations, including on their public and private funding, and membership, to the European Data Portal would contribute to the overall transparency of these entities.

Publish more than what is requested

Regulation 2025/2445 requires the publication of specific information and data, including in its Article 39. One way to understand this legal provision is that only the information explicitly listed in the Regulation should be published.

Another approach, which is more consistent with the goal of achieving transparency — recalled in recital 51, in Articles 10 and 11 of the Treaty on European Union, and in Article 15 of the Treaty on the Functioning of the European Union — is to consider these explicit requirements as a baseline for transparency, which can be expanded upon with the publication of other relevant data.

Explicit publication requirements should be considered a baseline for transparency.

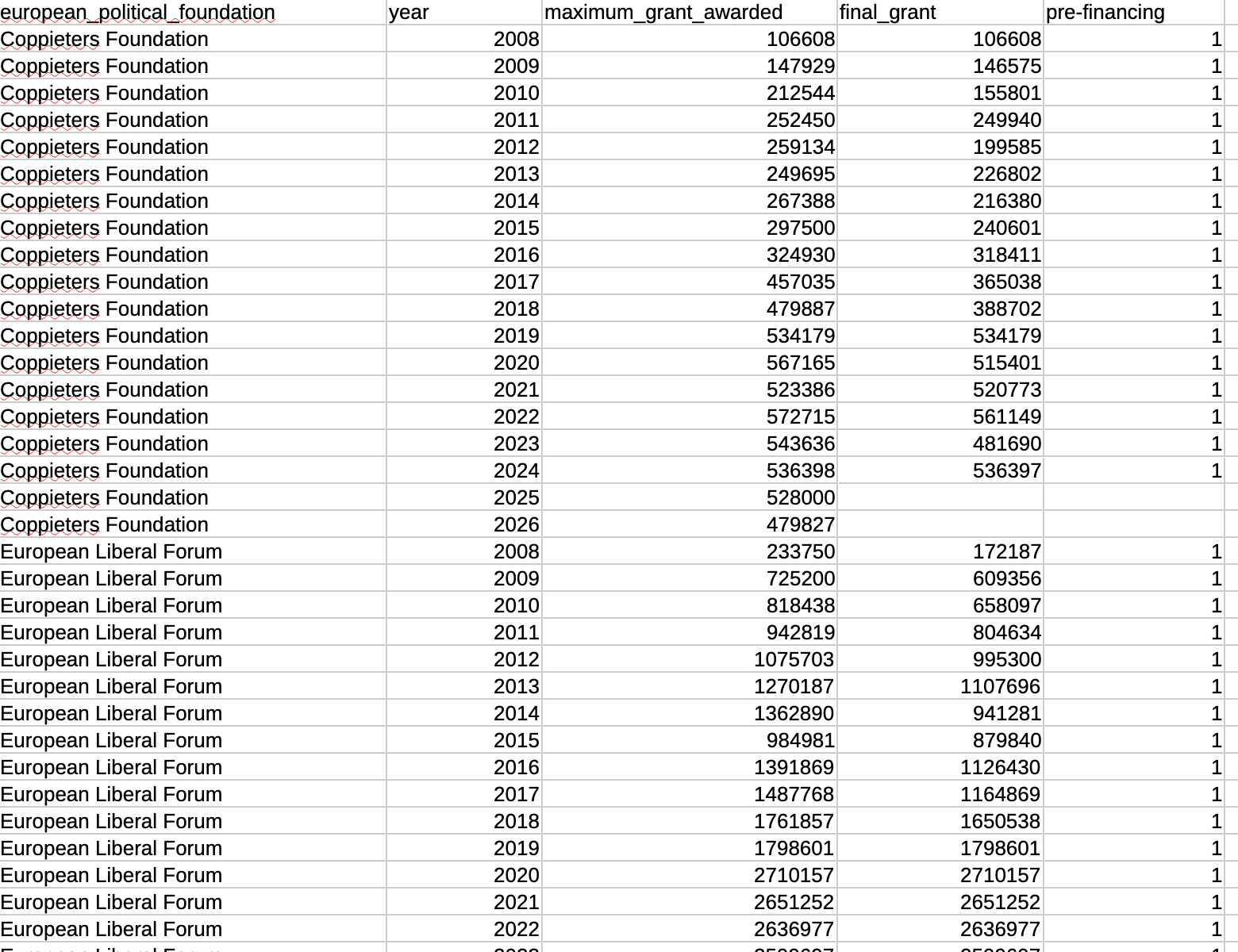

Over the years, the APPF and DG FINS have oftentimes opposed the publication of additional information and data, invoking a "data minimisation principle" and arguing that they had no explicit legal basis to publish this data, despite the treaty-recognition of a general principle of transparency. In some specific and limited cases, however, this has not prevented them from publishing data that was not explicitly required: for instance, there is not explicit requirement for DG FINS to publish the maximum entitlement of European parties and foundations, which it publishes alongside final grants, and there is no requirement for the APPF to publish the national identification numbers of legal entities in its publication of donations. These are two welcome initiatives.

Continuing in this direction, DG FINS, which publishes the amounts of public funding received by European parties and foundations, could publish the more detailed information about the calculations that have led to these amounts. This data can already be accessed by citizens but requires a request for access to documents; it could be proactively included in the data published by the European Parliament.

Similarly, the APPF could publish data on donations and contributions that predates its creation — this is data that was previously handled by the European Parliament, and that is accessible to citizens following a request for access to documents. Including this data in the APPF's own records would provide useful context to the APPF's more recent data on the funding of European parties and foundations.

Use a database instead of files

In a similar vein as the previous point, the APPF and DG FINS have often focused on documents instead of data. Since Article X.Y(z) requires the publication of a specific information, a document containing this information is prepared and published. This approach is understandable.

However, the requiments rarely mention the publication of a specific document, and instead refer to the publication of specifica data, such as names, donations, contributions, membership, etc. This document-based approach has also led to documents being periodically deleted from the website of the APPF, presumably to avoid the website from listing too many files, which regrettably limits transparency and prevents a historical perspective.

Already, transitioning to CSV files would allow for a streamlining of these documents. For instance, instead of publishing a new document every time a European party sees a change in its membership, a CSV file listing all membership records could simply add a new record when a national member joins, or add a membership end date when a national party's membership ends.

A database can form the core of an online reporting and disclosure system.

But an even more efficient way to ensure transparency would be to rely less on separate files, each containing one piece of information, and instead to build a database containing all data gathered on European parties and foundations. Representatives of reporting entities could then be granted rights to add or, in some cases, edit information from this database, and the database could directly lead to the publication of data on the website of the APPF or of the European Parliament.

Data on specific aspects, either as a whole or using relevant user filters, could then be extracted automatically into CSV or XML formats. This would avoid the need to manually handle files, and would form the core of an online reporting and disclosure system. This would simplify reporting for European parties and foundations, partially automate compliance monitoring for institutions and auditors, and enhance transparency for citizens.

Finally, creating a database allows the setting up of an application programming interface (API) which enables the automatic retrieval of data, removing the need for periodic exports when data is updated, which greatly facilitates the data expoitation flow.

Build infographics

Finally, while the disclosure of data in machine-readable format is essential for transparency and citizens' oversight, citizens are far more likely to be interested in — and to better understand — infographics than raw numbers.

This is why the European Parliament publishes charts of the results of European elections, together with datasheets in open, machine-readable format, for all elections since 1979. Or why the EPRS focuses on visualisations on its Facts and Figures website, always with the possibility to export the chart itself and its underlying data in various formats.

And it is the same reason the European Democracy Consulting Stiftung built the European Party Funding Observatory.

|  |

|---|

Likewise, instead of placing documents, or even data, front and center, the APPF and DG FINS should instead focus on the visualisation of their data, while ensuring that charts and their underlying data can be easily exported in a variety of open, machine-readable formats.

Examples

The guidance above ensures the proper implementation of the "open, machine-readable" requirement, and greatly enhances transparency. In this last section, we will put in practice this guidance, and provide examples of formatting for relevant documents listed in the Regulation.

While based on actual data, the values below are merely used as examples.

Total number of individual member

| european_party | year | member_state_iso2 | number_individual_members |

|---|---|---|---|

| ALDE | 2026 | AT | 0 |

| ALDE | 2026 | BE | 0 |

| ALDE | 2026 | BG | 1 |

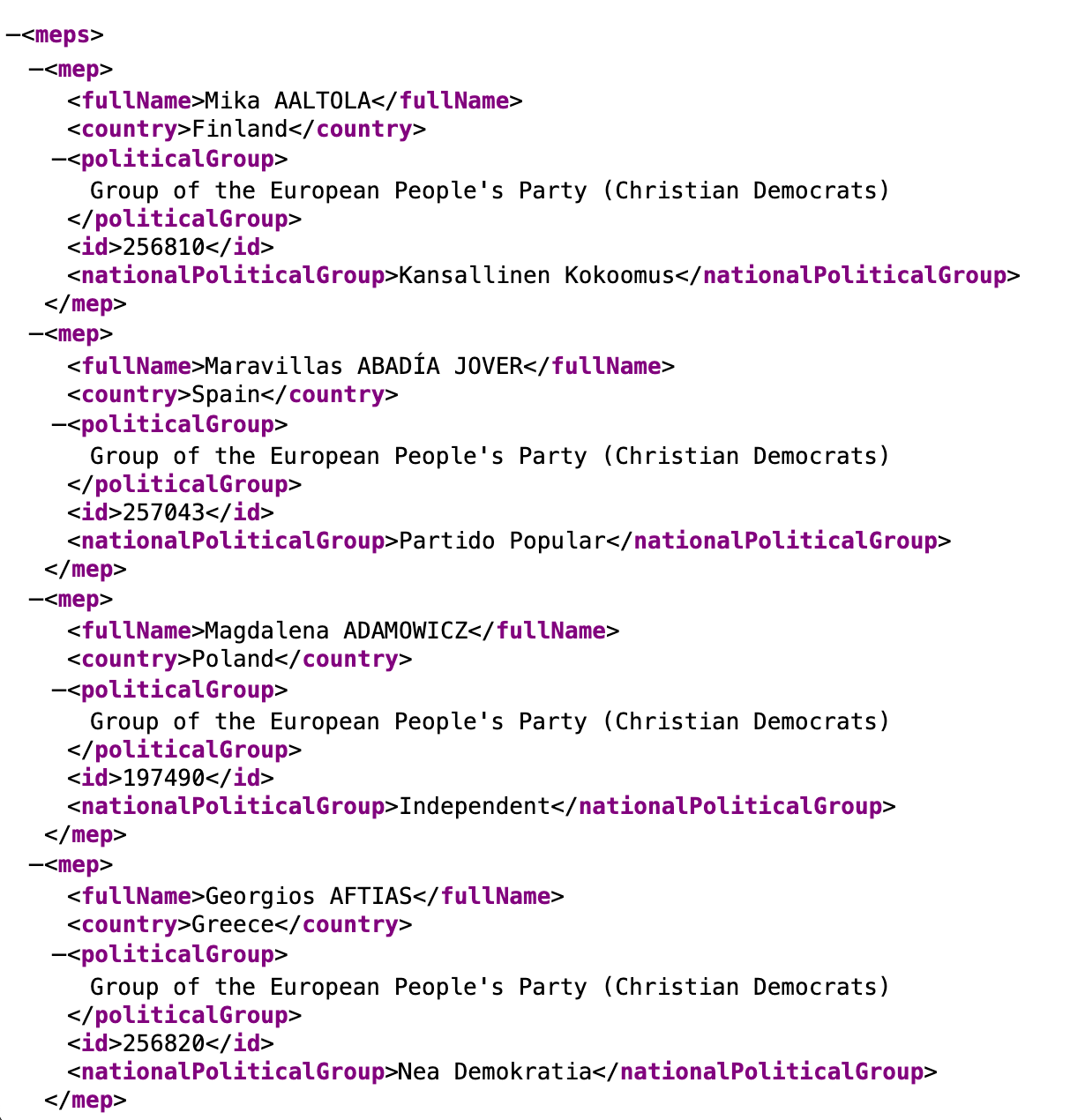

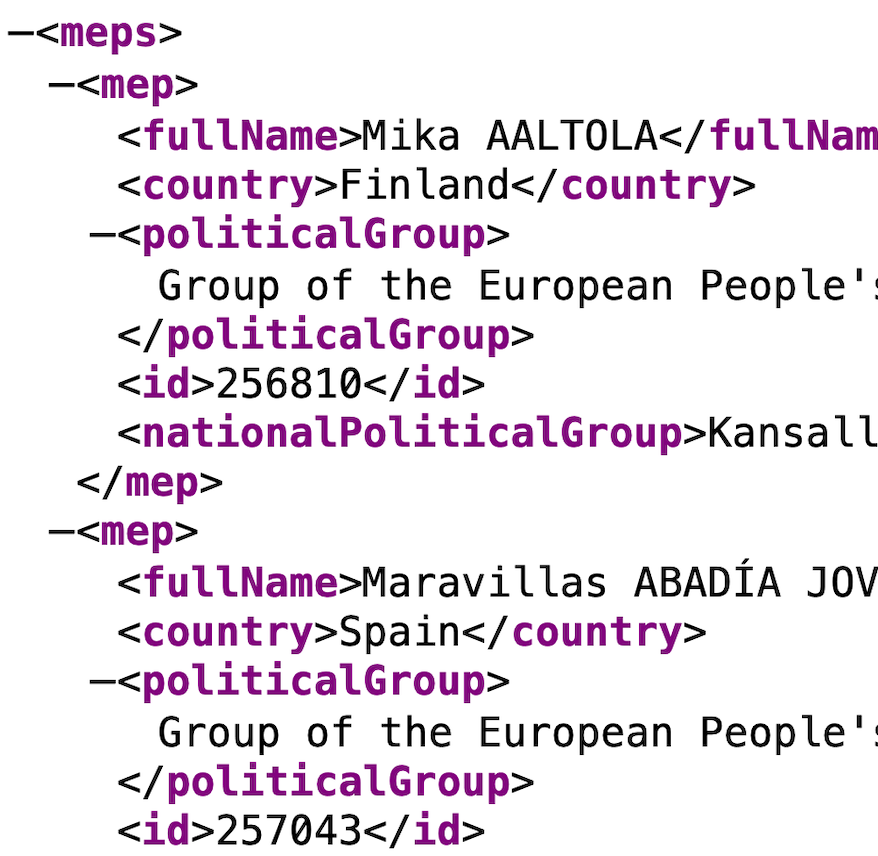

List of MEPs members of a European party

| european_party | last_name | first_name | ep_id | member_state_iso2 | date_membership_start | date_membership_end |

|---|---|---|---|---|---|---|

| EPP | AALTOLA | Mika | 256810 | FI | XXXX-XX-XX | |

| EPP | ABADÍA JOVER | Maravillas | 257043 | ES | YYYY-YY-YY | |

| EPP | ADAMOWICZ | Magdalena | 197490 | PL | ZZZZ-ZZ-ZZ | |

National party membership

| national_party_id | national_party_name | national_party_name_en | acronym | also_or_formerly_known_as | country_iso | european_party | membership_type | membership_status | date_membership_start | date_membership_end |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | NEOS – Das Neue Österreich und Liberales Forum | NEOS – The New Austria and Liberal Forum | NEOS | NEOS – The New Austria | AT | ALDE | full member | full | XXXX-XX-XX | |

| 2 | Die Volkspartei | Austrian People's Party | ÖVP | Die neue Volkspartei, Österreichische Volkspartei | AT | EPP | full member | full | YYYY-YY-YY | |

| 3 | Partidul Verde | Green Party | PV | RO | EGP | full member | suspended | ZZZZ-ZZ-ZZ | ||

| 4 | Partidul Social Democrat European | European Social Democratic Party | PSDE | Mișcarea pentru o Moldovă Democratică și Prosperă, MPMDP | MD | PES | observer member | full | AAAA-AA-AA | |

| 5 | PRO România | PRO Romania | PRO | RO | EDP | full member | full | BBBB-BB-BB | 2022-10-15 | |

| 5 | PRO România | PRO Romania | PRO | RO | PES | observer member | full | 2022-10-15 | ||

Public funding

| european_party | year | meps | lump_sum | mep_based_funding | grant_requested | elligible_expenditure_budget | public_funding_maximum_grant | pre-financing | elligible_expenditure_final | public_funding_final |

|---|---|---|---|---|---|---|---|---|---|---|

| ALDE | 2022 | 68 | 460000.00 | 4813953.49 | 5294539.00 | 5991500.00 | 5273953.00 | 1.00 | 6010500.00 | 5273953.00 |

| ECPP | 2022 | 5 | 460000.00 | 343853.82 | 966056.00 | 1073396.00 | 803854.00 | 1.00 | 978896.00 | 794255.00 |

Donors and contributors

| donor_contributor_id | donor_contributor_name | donor_contributor_name_en | acronym | national_registration_id | first_name | middle_name | last_name | donor_contributor_category | member_state_iso2 |

|---|---|---|---|---|---|---|---|---|---|

| 1 | Microsoft Belgium | Microsoft Belgium | BE0437910359 | private company | BE | ||||

| 2 | Microsoft Ireland | Microsoft Ireland | private company | IE | |||||

| 3 | Bayernpartei | Bavaria Party | BP | political party | DE | ||||

| 4 | Sarah | L. | Connor | individual | AT | ||||

Donations and contributions

| date | donor_id | recorded_as | donation_contribution_type | donation_amount | number_donors_contributors | donation_id | beneficiary |

|---|---|---|---|---|---|---|---|

| 2026-01-02 | 3 | Bayern Partei | member party contribution | 2000.00 | 1 | 26.01.3.1 | EFA |

| 2026-03-12 | 231 | Eli Lilly Benelux S.A | identified donation | 18000.00 | 1 | 26.03.231.1 | ALDE |

| 2026-05-09 | 3 | Bayern Partei | member party contribution | 8000.00 | 1 | 26.05.3.2 | EFA |

| 2025 | 9999 | Minor donors | minor donations | 3483.00 | 84 | 25.00.9999.1 | EGP |

Conclusion

By adding just a few words, the co-legislators have paved the way for a major improvement in transparency. At the same time, they have introduced a change which may prove difficult for some at the beginnning.

The European Democracy Consulting Stiftung is committed to enhancing transparency on European parties and foundations and their funding, as a way to better inform European citizens and strengthen European democracy. We welcome the steps already taken by European institutions to implement this new provision, and hope this guide will prove useful to their future work.

As always, we remain available by email or via our contact form for any further guidance and support, in line with our mission.

Resources

- European Data Portal, https://data.europa.eu/en

- Open Data Handbook, https://opendatahandbook.org/

- Open Knowledge, https://okfn.org/en/

- LibreOffice, https://www.libreoffice.org/

- Open Document Format, https://blog.documentfoundation.org/blog/2025/05/16/what-is-odf/